According to a recently released NPD DisplaySearch Quarterly Mobile PC Value Chain report, the increased adoption of tablets, the ongoing dominance of Apple in the mobile computing space generally, and the newly robust sales of Amazon and Google tablets - not to mention the emergence of Microsoft in the tablet space - are all converging to change the competitive landscape for screen/display manufacturers. In fact, all of the players in the supply chain here (display manufacturers, OEMs, and brands) for the mobile PC market - which includes notebooks, tablets, and ultra-slim PCs - have now modified their business strategies and allocation plans to leverage their strengths and maintain market share.

NPD DisplaySearch is a global market research and consulting firm that specializes in the display supply chain, as well as the emerging photovoltaic/solar cell industries. NPD DisplaySearch provides trend information, forecasts and analyses. NPD DisplaySearch is owned by The NPD Group, which provides global information and advisory services.

Jeff Lin, value chain Analyst at NPD DisplaySearch notes, “With the changes taking place in the mobile PC segment, existing supply chain relationships could be disrupted due to competitive conflicts. For example, Samsung Display plans to improve its mobile PC customer portfolio by reducing its share in Apple and increasing support to captive brands and other external customers, like Amazon and Barnes & Noble.”

Lin adds, “In addition, the shift to touch notebooks and ultra-slim PCs will be key areas of focus for Apple’s mobile PC competitors in 2013. While capturing a larger portion of these market segments will be challenging, competitors will require solid commitments from their supply chain vendors (panel suppliers and OEMs) to ensure capacity and fool-proof, cost-down solutions. For example, HP, Lenovo, Samsung, and Acer have slashed prices on their ultra-slim notebooks in the hopes of combatting the competition.”

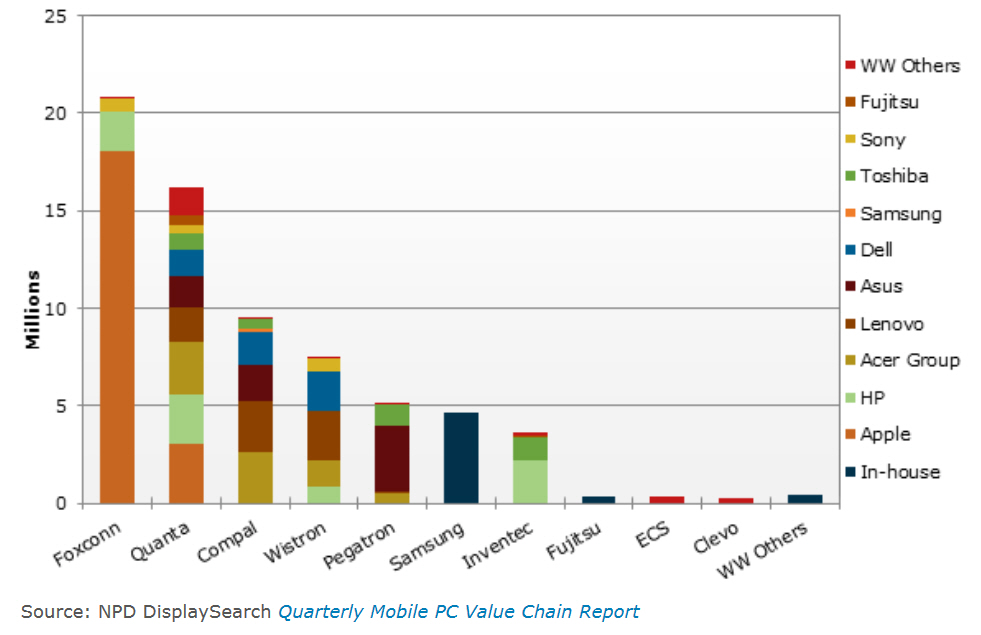

According to findings, LG Display led in mobile PC panel shipments in Q2 2012, with more than one third of its shipments going to Apple. Apple was the clear leader in the mobile PC market, with its tablet PC shipments accounting for 84 percent of total mobile PC shipments for the quarter. These were primarily manufactured by Foxconn.

Hewlett-Packard ranked second in the mobile PC category, with Quanta capturing the largest portion of HP’s overall production at about 33 percent. Foxconn led in mobile PC OEM production volume in Q2 2012, with more than 85 percent of its production volume coming from Apple’s new iPad (iPad 3) and iPad 2. In Q2 2012, Quanta started producing the Google seven inch Nexus tablet PC. The chart below shows how the major players rank relative to one another.

Lin continues: “With 2013 business planning well underway, product portfolios, sales strategies, and sourcing plans for mobile PC brands will certainly impact the supply chain. Overall, 2012 year over year growth rates for the top 10 PC brands are forecast to increase only 2 percent for notebook PCs and fall 28 percent for mini-notebook PCs. However, growth for tablet PCs is still reliably robust at 75 percent. Looking ahead to 2013, business plans for the top 10 PC brands are set higher, with a 16 percent year over year shipment increase on average for notebook PCs. Tablet PC growth will remain strong, but will likely be less impressive than in 2012.”

QUICK LINKS

QUICK LINKS